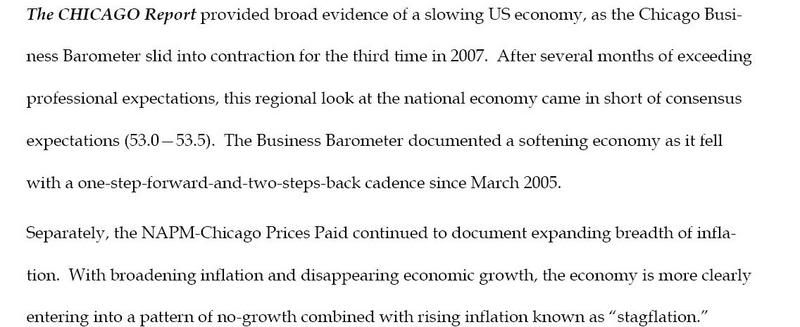

From the Federal Reserve:

Industrial production decreased 0.5 percent in October after having increased 0.2 percent in September. At 114.0 percent of its 2002 average, total industrial production in October was 1.8 percent above its year-earlier level. Output in the manufacturing sector fell 0.4 percent in October. The output of utilities dropped 1.6 percent, primarily because of a decline in gas utilities; the output at mines fell 0.6 percent, reversing September's gain. Capacity utilization for total industry declined to 81.7 percent, a rate equal to its year-earlier level but 0.7 percentage point above its 1972-2006 average.

.....

The output of consumer goods dropped 0.7 percent in October; the decreases were widespread

.....

The index for business equipment edged down 0.1 percent in October.

.....

In October, the index for construction supplies moved down 0.4 percent, its fourth consecutive monthly decline; nevertheless, the index remained 0.1 percent above its year-earlier level.

.....

The production of materials fell 0.4 percent in October after having risen 0.3 percent in September

Still, as this chart from Econoday indicates, overall industrial production is still positive.

This chart looks like the best way to describe US manufacturing is "fair". It could be higher, but we're still positive and still growing. My guess is foreign demand is really helping out with this figure.

From the Philadelphia Fed (November 15):

Activity in the region’s manufacturing sector continued to expand in November at about the same modest pace as in October, according to firms responding to this month’s Business Outlook Survey. Indicators for general activity and new orders remained positive and increased slightly from their readings last month. The employment index, while remaining positive, fell notably this month. Firms continued to report a rise in prices for inputs, and prices for the firms’ own manufactured goods have increased in recent months. The region’s manufacturing executives were substantially less optimistic about future activity than they were in October, and responses to special questions indicated that some firms are cutting back on fourth-quarter production plans.

This, again, looks like a "fair" report. There are two causes for concern. The first is the decrease in employment. This could indicate companies are looking to scale back costs. Secondly, the prices paid for inputs category is increasing. I am always suspicious of future predictions and tend to discount them regardless of the overall sentiment.

From the NY Fed (November 15):

The Empire State Manufacturing Survey indicates that conditions for New York manufacturers improved in November, at a pace close to that observed in October. The general business conditions index held steady at 27.4. The new orders and shipments indexes were also elevated and near last month’s levels. The prices paid index rose to its highest level in more than a year, while the prices received index was less elevated and declined modestly. Employment indexes, though positive, were markedly lower than in October. The degree of optimism regarding conditions six months ahead deteriorated: future activity indexes remained positive but dropped noticeably. The future prices paid index rose sharply to its highest level in considerably more than a year.

Here's the accompanying chart:

I would also classify this report as fair. The accompanying chart indicates overall conditions are fine; they're at levels seen in 2004, 2005 and 2006. Again we see a decline in the employment number. This is consistent with the Philly survey and could indicate a shift in business sentiment. However, one month is not a trend and we need more data before we draw a firm conclusion.

On October 31, the NAPM index dropped to 49 (PDF). New orders dropped as well. Here's the report's conclusion:

This conclusion is a cause for concern.

From the Kansas Fed (October 25):

Tenth District manufacturing output expanded modestly in October, and producers remained largely positive about future activity. However, orders and employment indexes were sluggish, and firms continued to trim inventories. Most price indexes in the survey edged up slightly.

Once again we see employment as "sluggish." That's the third district that has made a negative comment about employment.

Richmond Fed (October 23):

Manufacturing activity pulled back in October; Shipments and new orders decrease; But expectations upbeat

Manufacturing activity in the central Atlantic region pulled back in October, after expanding during the previous four months, according to the Richmond Fed’s latest survey. The index of overall activity was pushed lower as shipments and new orders edged into negative territory. Most other indicators also suggested weaker activity. District contacts reported that the pace of hiring flattened, order backlogs declined further and delivery times grew more slowly. Furthermore, manufacturers reported that capacity utilization reversed its positive reading seen last month and that inventories grew at a slightly slower pace.

Despite the decline in activity, manufacturers were more optimistic about their future prospects in October. Firms anticipated that their shipments, new orders, capacity utilization and employment would grow more rapidly in the months ahead.

While this index dropped, it did so after four months of increases. This looks more like a natural pullback rather than a problem.

The overall read I get from all of these reports is "fair" with cause for concern. The national number could be higher but is still expanding. While the latest figures showed a drop, it is only one month of information and the year over year chart still shows an expansion.

The regional reports are mixed, and three indicated that employment was a concern. This could be an indication that companies are looking to cut back on labor, which is never a good sign.